Buying your first home is both exciting and stressful. The process can feel overwhelming, especially when you see the prices and hear about the need for a big down payment. Thankfully, first time home buyer loan programs exist to make homeownership possible—even if you do not have perfect credit or a lot of cash saved. These programs give you support, lower costs, and make your dream of owning a home much more real.

Many people believe you need 20% down and high income to buy a home. That is simply not true. With the right loan program, you can get into a house with much less money, and sometimes with help from the government or local agencies.

But knowing which program fits your needs can be confusing if you are just starting out. This guide explains the main types of loans, breaks down their requirements, and gives you tips that most beginners miss. You will learn how to avoid common mistakes and make a confident decision.

What Is A First Time Home Buyer Loan Program?

A first time home buyer loan program is a mortgage (home loan) designed to help people who have never owned a home or have not owned one in the past three years. These programs often give you:

- Lower down payments

- Reduced interest rates

- Help with closing costs

- Easier credit requirements

They are offered by federal and state governments, local agencies, and even some banks. The goal is to make buying a home affordable, especially for those with lower income or savings.

Main Types Of First Time Home Buyer Loan Programs

Not all home loans are the same. Here are the most popular options for first time buyers in the United States.

1. Fha Loans

FHA loans are backed by the Federal Housing Administration. They are one of the most common choices for first-time buyers.

- Down payment: As low as 3.5% if your credit score is 580 or higher.

- Credit score: Minimum 500 (with 10% down); 580 for 3.5% down.

- Mortgage insurance: Required, both upfront and monthly.

- Property type: Must be your main home.

FHA loans are popular because they are flexible. If you have a lower credit score or a smaller down payment, FHA could work for you. One thing many people miss: FHA loans require you to pay mortgage insurance for the life of the loan unless you refinance or put at least 10% down and wait 11 years.

2. Conventional 97 Loans

The Conventional 97 is a special low-down-payment program from Fannie Mae and Freddie Mac.

- Down payment: Only 3%.

- Credit score: Typically 620 or higher.

- Mortgage insurance: Required, but drops when you reach 20% equity.

- Income limits: May apply.

Unlike FHA, conventional loans do not have upfront mortgage insurance, and the monthly insurance can be cancelled once you have enough equity. Many first-time buyers do not realize that conventional loans can be a better deal long-term if your credit is strong.

3. Va Loans

If you are a veteran, active-duty military member, or eligible spouse, a VA loan from the Department of Veterans Affairs is one of the best options.

- Down payment: 0% (no down payment needed).

- Credit score: Flexible, but most lenders want at least 620.

- Mortgage insurance: None, but there is a one-time VA funding fee.

- Other benefits: No loan limits, competitive rates, fewer closing costs.

Many military families miss out on VA loans because they think they need to use it only once. You can actually use it more than once in your lifetime.

4. Usda Loans

USDA loans are backed by the U.S. Department of Agriculture for buyers in rural and some suburban areas.

- Down payment: 0%.

- Credit score: Around 640 or higher.

- Income limits: Yes, based on area and family size.

- Location: Must be in an eligible rural area.

These loans are not just for farmers. Many small towns and even some suburbs qualify. If you want a home outside a big city, this loan can save you a lot of money.

5. State And Local Programs

Each state and many cities offer their own first-time buyer programs. These can include low-interest loans, down payment grants, or help with closing costs.

- Down payment assistance: Grants or loans to help with cash needed.

- Special programs: For teachers, police, nurses, or people in certain neighborhoods.

- Requirements: Usually income and home price limits.

These programs are often underused because people simply do not know they exist. Always check with your state or local housing office to see what is available.

Comparing The Main Loan Programs

To help you see the differences, here’s a side-by-side look at the four main federal loan programs:

| Loan Program | Minimum Down Payment | Mortgage Insurance | Credit Score Needed | Special Limits |

|---|---|---|---|---|

| FHA | 3.5% | Required | 500–580+ | Loan limits by area |

| Conventional 97 | 3% | Required, can cancel | 620+ | May have income limits |

| VA | 0% | Not required | Flexible (620+) | Must have VA eligibility |

| USDA | 0% | Required | 640+ | Income & area limits |

Key Benefits Of First Time Home Buyer Loans

First time buyer loans are not just about the down payment. Here are some reasons why these programs are so valuable:

- Lower upfront costs: You do not need to save tens of thousands for a down payment.

- More flexible credit rules: Even if your credit is not perfect, you may still qualify.

- Assistance with closing costs: Some programs help pay for fees at closing.

- Education and support: Many require a homebuyer education class, which teaches you about budgeting, the buying process, and maintaining your home.

- Grants and forgivable loans: Some programs give you money that you do not have to pay back if you live in the home long enough.

A non-obvious insight: Some programs can be combined. For example, you might use an FHA loan and get down payment assistance from your city or state. This can reduce your costs even further.

Common Mistakes First-time Buyers Make

Buying a home is a big deal, and it is easy to make mistakes. Here are some things to watch out for:

- Skipping pre-approval: Always get pre-approved before you shop. It shows sellers you are serious and tells you what you can really afford.

- Ignoring extra costs: Your monthly payment is not just the loan. You will also pay for taxes, insurance, and possibly homeowner association (HOA) fees.

- Not shopping around: Different lenders offer different rates and fees. Compare at least three lenders.

- Missing local programs: Many people miss out on grants or assistance because they do not check state and city options.

- Stretching your budget: Just because you qualify for a certain amount does not mean you should borrow that much. Leave room in your budget for emergencies.

Many buyers also do not realize that some loans (like FHA) require the house to meet certain standards. If you want a fixer-upper, you need to check if your loan allows it.

How To Qualify As A First Time Home Buyer

You do not have to be a “true” first time buyer. Most programs consider you first time if you have not owned a home in the past three years. Here’s what you usually need:

- Proof of income: Pay stubs, tax returns, or other income statements.

- Decent credit: The higher your score, the better your rate, but low scores may still qualify.

- Down payment funds: Even if it is only 3% or comes from a gift or grant.

- Stable job: Most lenders want to see at least two years of work history.

- Low debt-to-income ratio: Your monthly debts compared to income should be under 43% for most programs.

A tip most people miss: You can use gifted money for your down payment or closing costs, but you must document where it came from. Lenders need proof it is not a loan.

Practical Steps To Get Started

Ready to buy? Here is how to move forward:

- Check your credit report: Make sure there are no mistakes. A higher score means a lower rate.

- Estimate your budget: Use online calculators to see what you can afford, including taxes and insurance.

- Save for upfront costs: Besides your down payment, you will need money for inspections, appraisals, and moving.

- Research programs in your area: Many states have their own websites listing all available assistance.

- Get pre-approved: Talk to at least two or three lenders. Ask about all first time buyer programs they offer.

- Take a homebuyer education course: Many programs require this. It is usually low-cost or free and can save you from costly mistakes.

- Work with a trusted real estate agent: Choose someone who has experience with first time buyers and knows local programs.

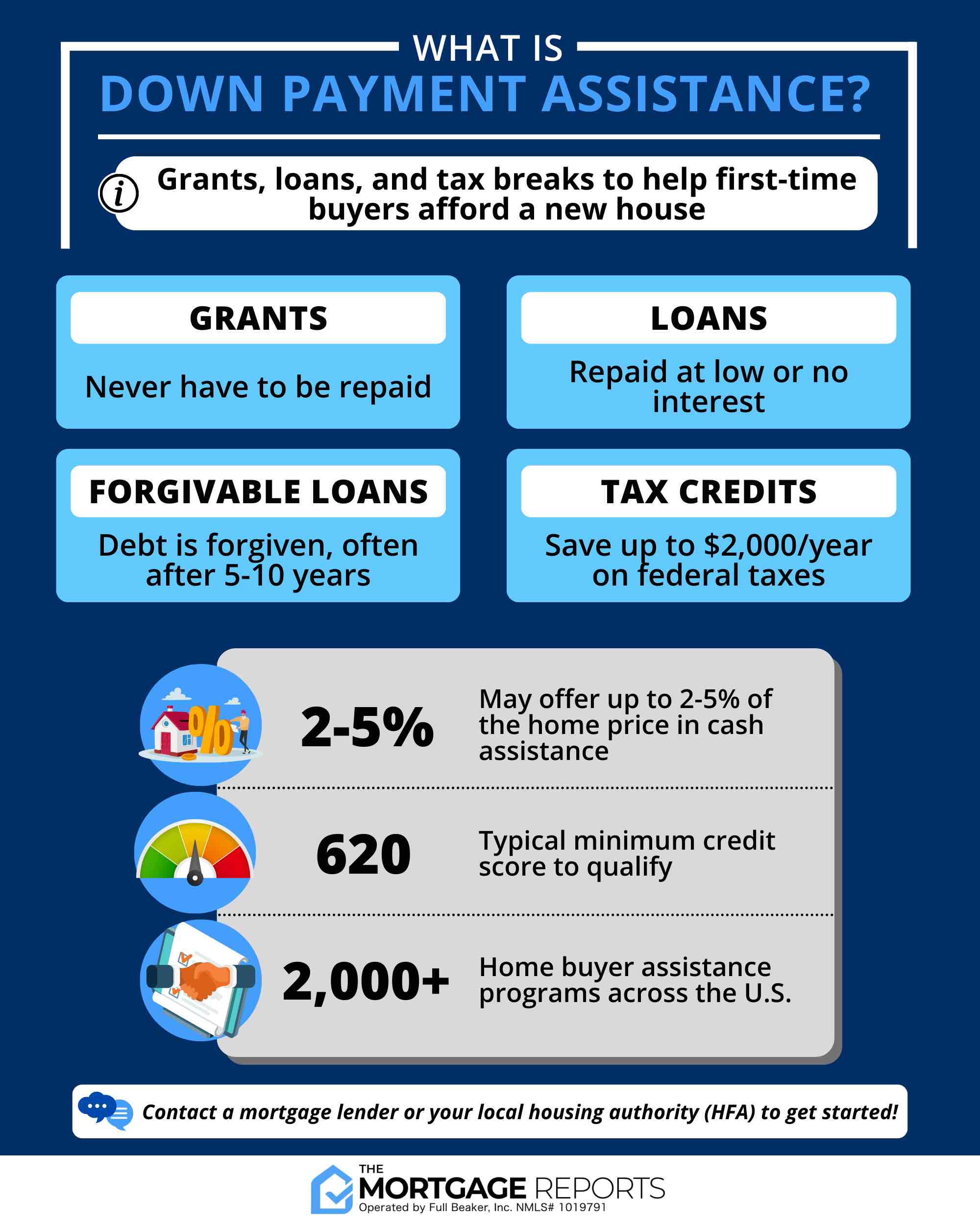

How Down Payment Assistance Works

Down payment assistance (DPA) can be a grant, a forgivable loan, or a low-interest second loan. Here’s a quick comparison:

| Type | Repayment | Typical Amount | Best For |

|---|---|---|---|

| Grant | Not repaid | $1,000–$10,000 | Those who meet income limits |

| Forgivable Loan | Forgiven after 5–15 years | $2,500–$20,000 | Staying in home long-term |

| Deferred Loan | Paid when home is sold | $5,000–$15,000 | Those who expect to move |

Many buyers do not know that accepting DPA may add extra paperwork or time to the process. Always ask your lender how it will affect your timeline.

Understanding Closing Costs

Closing costs are the fees you pay to complete the purchase. They include:

- Loan origination fees

- Appraisal and inspection costs

- Title insurance

- Prepaid taxes and insurance

- Recording fees

These costs usually total 2% to 5% of the purchase price. Some loan programs or local agencies will help pay part of these costs, but you must ask.

Real-world Example

Let’s say you want to buy a $300,000 home. Here’s how the numbers might look with an FHA loan:

- Down payment: 3.5% of $300,000 = $10,500

- Closing costs (3%): $9,000

- Total cash needed: $19,500

If you get a $5,000 grant from your city, that lowers your needed cash to $14,500. Add in a gift from family or a forgivable loan, and your upfront costs may drop even more.

Credit Scores: Why They Matter

Your credit score affects the interest rate you pay and which programs you can use. Here is a quick look at the impact:

| Credit Score | Loan Type Available | Estimated Rate |

|---|---|---|

| 760+ | All programs | Best rates (5.5%–6%) |

| 700–759 | Most programs | Good rates (6%–6.5%) |

| 620–699 | FHA, VA, some conventional | Higher rates (6.5%–7%) |

| 500–619 | FHA (with more down) | Highest rates (7%+) |

If your score is below 620, you may need to work on your credit before applying. Pay down debts and do not open new credit cards right before you buy.

Where To Find More Information

To find programs in your area, visit the HUD website, your state’s housing agency site, or talk to a local lender. The Consumer Financial Protection Bureau also offers trusted advice for first time buyers.

Frequently Asked Questions

What Is The Minimum Credit Score For First Time Home Buyer Loans?

Most programs require a score of at least 580 for FHA (3.5% down), 620 for conventional loans, and 640 for USDA. VA loans are flexible, but most lenders want 620 or higher.

Can I Buy A Home With Zero Down Payment?

Yes, VA and USDA loans offer 0% down options. Some local programs also provide down payment grants that can cover your minimum requirement.

Are There Programs For Buyers With Low Income?

Absolutely. Many state and local programs are designed for low- and moderate-income families. Income limits vary by location and family size.

Do I Need To Pay Back Down Payment Assistance?

It depends. Grants usually do not need to be repaid. Forgivable loans are wiped out if you stay in the home for a set time. Deferred loans are paid when you sell or refinance.

How Long Does It Take To Buy A Home With These Programs?

The process can take 30–60 days, depending on the program and how quickly you get documents to your lender. Using down payment assistance may add a week or two to the process.

Buying your first home is a big step, but you do not have to do it alone. With the right first time home buyer loan program, you can make homeownership possible—sometimes sooner than you think. Take your time, ask questions, and choose the program that fits your budget and your life.

You will be glad you did.

Read More:

- Best Personal Finance Software: Top Picks to Manage Your Money

- Financial Planning Advisor Near Me: Find the Best Local Experts

- Best Investment Apps for Beginners: Top Picks for 2024

- Retirement Planning Calculator Online: Secure Your Future Today

- Wealth Management Services for Beginners: Your Essential Guide

- Small Business Loan Pre Approval: Boost Your Funding Success

- Best Personal Loan Rates: How to Secure the Lowest APRs Today

- Home Equity Loan Rates Comparison: Find the Best Deals Today