Finding the Best Personal Loan Rates: What You Need to Know

Personal loans can help you pay for big expenses, consolidate debt, or handle emergencies. But getting a loan with the best rates can save you a lot of money over time. This guide explains how personal loan rates work, what affects them, and how you can find the lowest rates for your situation. Whether you’re new to borrowing or want to improve your approach, you’ll find clear advice and practical tips here.

What Are Personal Loan Rates?

Personal loan rates are the interest percentages lenders charge on the money you borrow. These rates affect how much you’ll repay each month and in total. Most personal loans have fixed rates, meaning your payments stay the same for the life of the loan. Some loans have variable rates that can change, but these are less common.

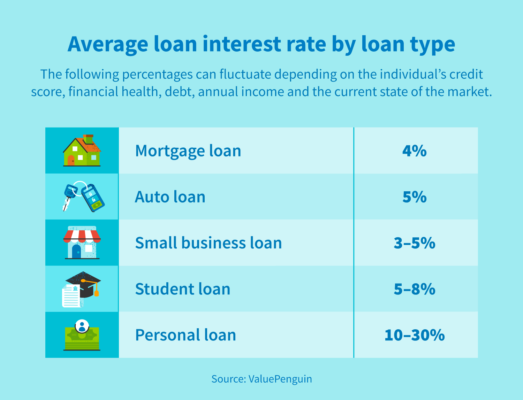

Interest rates for personal loans usually range from 6% to 36%. The rate you get depends on your credit score, income, debt-to-income ratio, and other factors. Even a small difference in rates can mean hundreds or thousands of dollars saved or spent over the loan term.

Why Interest Rates Matter

A lower interest rate means lower monthly payments and less money paid over time. For example, if you borrow $10,000 with a 36-month term:

| Interest Rate | Monthly Payment | Total Interest Paid |

|---|---|---|

| 8% | $313 | $1,259 |

| 18% | $362 | $3,046 |

| 28% | $409 | $4,742 |

As you can see, the higher the rate, the more you pay. So, finding the best personal loan rates is important, especially if you borrow larger amounts.

How Lenders Decide Your Rate

Lenders look at several factors before offering you a rate. Understanding these can help you improve your chances of getting a better deal.

- Credit Score: The higher your score, the lower your rate. Most lenders require a score of at least 600 for standard loans, but rates drop significantly for scores above 700.

- Income: Lenders want to see stable and adequate income. This shows you can repay the loan.

- Debt-to-Income Ratio: If you already owe a lot compared to your income, lenders may offer higher rates or deny your application.

- Loan Amount and Term: Larger loans and longer terms often mean higher rates.

- Employment History: Stable employment can help you qualify for better rates.

Some lenders also consider location, education, or even your savings. Don’t assume that only your credit score matters.

Comparing Personal Loan Rates: Major Lenders

Different lenders offer different rates. Here’s a comparison of popular US lenders:

| Lender | APR Range | Minimum Credit Score | Loan Amounts |

|---|---|---|---|

| LightStream | 6.99%–24.99% | 660 | $5,000–$100,000 |

| SoFi | 8.99%–25.81% | 680 | $5,000–$100,000 |

| Marcus by Goldman Sachs | 6.99%–24.99% | 660 | $3,500–$40,000 |

| Upgrade | 8.49%–35.99% | 580 | $1,000–$50,000 |

| Discover | 7.99%–24.99% | 660 | $2,500–$40,000 |

Rates change often, and each lender uses their own criteria. Always check current offers before applying.

Tips To Get The Best Personal Loan Rates

- Check Your Credit Report: Review your credit report for errors. Correcting mistakes can quickly improve your score.

- Improve Your Credit Score: Pay down debts, make payments on time, and avoid new credit applications before applying for a loan.

- Shop Around: Get quotes from multiple lenders. Use “prequalification” tools, which show you possible rates without affecting your credit.

- Consider Credit Unions: These often offer lower rates than big banks, especially for members with good standing.

- Shorter Loan Terms: Choosing a shorter repayment period usually means lower rates.

- Avoid Extra Fees: Look for loans with no origination or prepayment fees. These can add to your total cost.

Many borrowers miss the chance to negotiate. If you have a strong credit profile, ask lenders if they can beat competitors’ offers. Even a small reduction can make a big difference.

Fixed Vs. Variable Rates

Most personal loans have fixed rates. This means your payment stays the same every month. Variable rates can change with the market, so your payment may go up or down.

Fixed rates are best for budgeting because you know exactly what you’ll pay. Variable rates can be risky, especially if interest rates rise. Some online lenders offer both options, but fixed rates are more popular.

The Role Of Fees And Apr

Interest rate is only part of the cost. APR (Annual Percentage Rate) includes interest and fees, showing the true cost of the loan.

Common fees include:

- Origination Fee: 1%–8% of the loan amount, charged upfront.

- Late Payment Fee: Charged if you miss a payment.

- Prepayment Penalty: Some loans charge you for paying off early.

Always compare loans by APR, not just interest rate. Two loans with the same interest rate can have very different APRs because of fees.

Here’s an example:

| Loan Amount | Interest Rate | Origination Fee | APR |

|---|---|---|---|

| $10,000 | 10% | 0% | 10.0% |

| $10,000 | 10% | 5% | 12.3% |

A loan with a higher APR can cost much more, even if the interest rate looks good.

How To Compare Offers

When comparing personal loans, focus on these points:

- APR: Includes all costs.

- Loan Term: Shorter terms mean less interest paid.

- Monthly Payment: Make sure you can afford it.

- Total Cost: Add up all fees and interest.

- Flexibility: Can you change your payment date or pay off early?

Many online tools let you compare offers side-by-side. Make sure to use reliable sources and read reviews. For accurate information, visit trusted sites like Consumer Financial Protection Bureau.

Real-world Examples

Let’s look at two borrowers:

Sarah has a credit score of 780. She borrows $15,000 for 3 years. Her rate is 7%. She pays $463 per month and about $1,690 in interest.

Mike has a score of 620. He borrows the same amount and term. His rate is 22%. He pays $574 per month and about $6,658 in interest.

These examples show how your credit score affects your loan cost. Improving your score before applying can save you thousands.

Common Mistakes When Looking For Low Rates

Borrowers often make these mistakes:

- Ignoring APR: Focusing only on interest rate leads to surprises from fees.

- Not Shopping Around: Accepting the first offer can mean missing better deals.

- Applying with Too Many Lenders: Each hard inquiry can lower your score.

- Borrowing More Than Needed: Larger loans mean higher rates and more interest.

- Overlooking Credit Unions: These often offer better rates, but many people stick with big banks.

A less obvious mistake is not checking if the loan is unsecured or secured. Secured loans (using collateral) can offer lower rates, but you risk losing your asset if you fail to pay.

Alternatives To Personal Loans

Personal loans aren’t always the best option. Consider these alternatives:

- Balance Transfer Credit Cards: Can offer 0% APR for 12–18 months, good for debt consolidation.

- Home Equity Loans: Lower rates but require property as collateral.

- Peer-to-Peer Lending: Sometimes lower rates, but less protection.

- Family Loans: No interest, but can risk relationships.

If you need a small amount and have a good credit score, a credit card might be cheaper for short-term needs.

When To Avoid Personal Loans

Personal loans are not ideal if:

- You need ongoing access to funds (consider a line of credit).

- Your credit score is very low (rates will be high).

- You cannot afford the monthly payment.

Some lenders advertise “guaranteed approval” or “no credit check.” These offers often come with very high rates and hidden fees. Avoid them unless you understand all risks.

Frequently Asked Questions

What Is A Good Interest Rate For A Personal Loan?

A good rate is usually below 10% for borrowers with strong credit. Average rates are around 12%–16% for most people. If your rate is above 20%, consider improving your credit or shopping around.

How Do I Get The Best Personal Loan Rates?

Improve your credit score, compare offers from multiple lenders, and look for loans with low fees. Sometimes joining a credit union can get you better rates.

Does Applying For A Personal Loan Affect My Credit Score?

Yes, most applications cause a hard inquiry on your credit report, which can lower your score slightly. “Prequalification” checks do not affect your score.

Can I Negotiate My Personal Loan Rate?

Sometimes. If you have a strong credit profile or competing offers, ask the lender to match or beat the rate. Not all lenders will negotiate, but it’s worth trying.

What Happens If I Miss A Payment?

Missing a payment can lead to late fees and lower your credit score. If you struggle to pay, contact your lender right away. Some offer hardship programs or payment plans.

Choosing the best personal loan rates requires careful comparison and an understanding of your own finances. By focusing on APR, improving your credit, and avoiding common mistakes, you can find a loan that fits your needs and budget. Remember: the lowest rate is not always the best if the fees are high or the terms are inflexible. Take your time, use trusted resources, and aim for the most affordable option available.

Read More:

- Best Personal Finance Software: Top Picks to Manage Your Money

- Financial Planning Advisor Near Me: Find the Best Local Experts

- Best Investment Apps for Beginners: Top Picks for 2024

- Retirement Planning Calculator Online: Secure Your Future Today

- Wealth Management Services for Beginners: Your Essential Guide

- Small Business Loan Pre Approval: Boost Your Funding Success

- Home Equity Loan Rates Comparison: Find the Best Deals Today

- Debt Consolidation Loan Online: Simplify Your Finances Today