Buying a home is often the biggest investment people make in their lives. Over time, as you pay off your mortgage, your home gains value and you build home equity. Many homeowners use this equity to get a loan for renovations, debt consolidation, or major purchases. But one question always comes up: Are you getting the best home equity loan rates? With rates changing from lender to lender and depending on your credit, comparing options can feel confusing. This guide will help you understand the basics, compare rates, and make smarter choices.

What Is A Home Equity Loan?

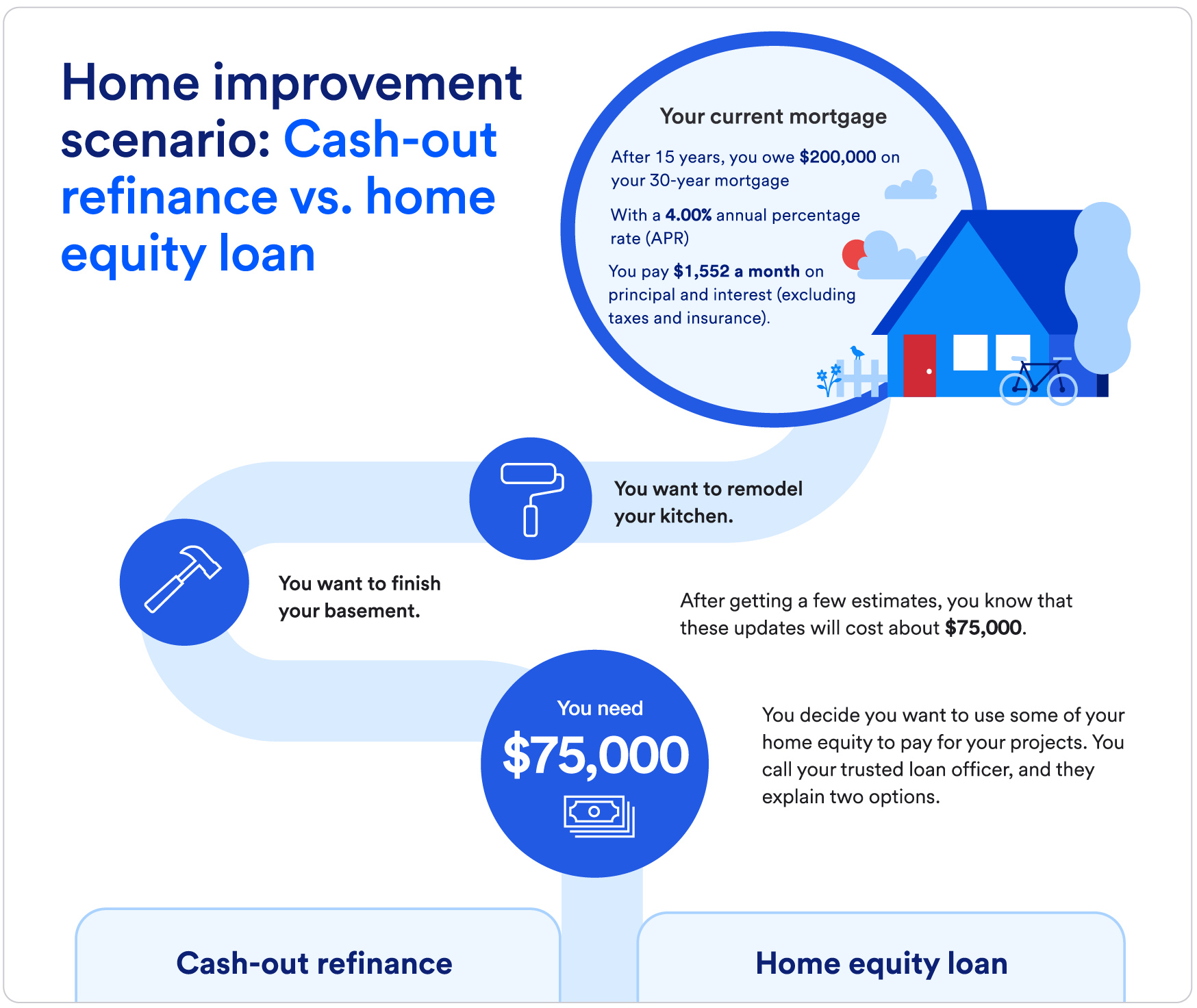

A home equity loan lets you borrow money based on the value of your home minus what you still owe on your mortgage. You get a lump sum with a fixed interest rate and pay it back in monthly installments. Unlike a home equity line of credit (HELOC), which works like a credit card, a home equity loan is straightforward: one loan, one rate.

Homeowners use these loans for:

- Home improvements (like remodeling kitchens)

- Debt consolidation

- Education expenses

- Emergency costs

The loan is secured by your home, so if you can’t pay, you risk foreclosure. That’s why getting a good rate is so important.

Factors Affecting Home Equity Loan Rates

Home equity loan rates aren’t the same for everyone. Here’s what lenders look at:

- Credit score: Higher scores mean lower rates. Most lenders want at least a 620.

- Loan-to-value (LTV) ratio: The more equity you have, the better your rate.

- Debt-to-income (DTI) ratio: If your debts are high compared to your income, your rate goes up.

- Loan amount and term: Bigger loans or longer terms may have higher rates.

- Location: State laws and local markets affect rates.

- Lender policies: Some banks or credit unions offer better deals to members.

For example, someone with an 800 credit score might get a rate near 7%, while a person with a 650 score could see rates above 10%.

Comparing Home Equity Loan Rates: 2024 Snapshot

Rates change often. In 2024, most lenders offer home equity loan rates between 7% and 11% for fixed-rate loans. Here’s a quick look at how different lenders stack up:

| Lender | Fixed Rate (APR) | Minimum Credit Score | Max LTV |

|---|---|---|---|

| Bank of America | 7.25% | 660 | 85% |

| Wells Fargo | 7.75% | 680 | 80% |

| Navy Federal Credit Union | 8.00% | 620 | 90% |

| U.S. Bank | 7.50% | 700 | 80% |

| Citibank | 7.90% | 660 | 85% |

Rates can also change if you’re a longtime customer or if you set up automatic payments.

Fixed Vs. Variable Rates

Most home equity loans have fixed rates. This means your payment stays the same every month. Some lenders offer variable rates, which can change over time. Fixed rates are safer if you want predictable payments, while variable rates can start lower but may rise later.

Here’s a simple comparison:

| Type | Starting Rate | Rate Changes? | Best For |

|---|---|---|---|

| Fixed | 7.5%–9.5% | No | Budgeting, long-term stability |

| Variable | 6.5%–8.0% | Yes | Short-term loans, risk-tolerant borrowers |

Most homeowners choose fixed rates for security. However, if you plan to pay the loan off quickly, a variable rate might save money in the first year.

Hidden Costs And Fees

The interest rate is only part of the story. Many loans include other costs:

- Origination fee: 0.5%–2% of the loan amount

- Appraisal fee: $300–$500 to check your home’s value

- Closing costs: Often $500–$2,000

- Prepayment penalty: Some lenders charge if you pay off early

Always ask for a breakdown of fees before signing. Sometimes, a loan with a lower rate but higher fees ends up costing more. This is a mistake many beginners make — focusing only on the interest rate and forgetting to check total costs.

How To Find The Best Rate

Getting the best home equity loan rate takes some work. Here’s a practical approach:

- Check your credit score: Clean up any errors before applying.

- Calculate your LTV ratio: Divide your remaining mortgage by your home’s value.

- Research at least 3–5 lenders: Look at banks, credit unions, and online lenders.

- Compare APR, not just interest rate: APR includes fees.

- Ask about discounts: Sometimes you get a lower rate for automatic payments or being a member.

- Read reviews and ratings: Check how lenders treat customers.

- Negotiate: If you have strong credit, ask for a better deal.

Here’s how APR can vary depending on fees:

| Interest Rate | Fees | APR |

|---|---|---|

| 7.5% | $1,500 | 8.1% |

| 8.0% | $500 | 8.2% |

| 7.9% | $2,000 | 8.6% |

Notice that a lower interest rate isn’t always the best deal if fees are high.

Real-life Example: Comparing Offers

Let’s say you have a home worth $400,000 and a mortgage balance of $250,000. Your equity is $150,000. You want to borrow $50,000 for a home remodel.

You check three lenders:

- Lender A: 7.5% fixed rate, $1,000 fees

- Lender B: 8.0% fixed rate, $500 fees

- Lender C: 7.8% variable rate, $800 fees

If you plan to pay over 10 years, the lower fixed rate (Lender A) is likely best, even with higher fees. But if you pay off in 2–3 years, Lender C’s variable rate could save you money in the short term.

Key insight: Always estimate your total interest plus fees for your planned loan term. Many people skip this step and regret it later.

Credit Unions Vs. Banks Vs. Online Lenders

Different lenders offer different rates and benefits:

- Credit unions: Often lower rates, especially for members. Flexible rules.

- Big banks: Reliable, but sometimes higher rates. Good for existing customers.

- Online lenders: Fast approval, sometimes competitive rates, but watch for hidden fees.

Some credit unions allow higher LTV ratios, meaning you can borrow more. Online lenders may approve loans faster, but you need to check their reputation.

Tips For Improving Your Rate

Want a better rate? Try these steps:

- Increase your credit score: Pay bills on time, reduce debt, fix errors.

- Lower your DTI ratio: Pay off debts before applying.

- Boost your home’s value: Small upgrades can increase appraisal value.

- Shop around: Don’t settle for the first offer.

- Join a credit union: Membership can unlock better rates.

Another tip: Some lenders offer “rate locks.” If rates are rising, locking in your rate early can save money.

Common Mistakes When Comparing Rates

Many homeowners make avoidable errors:

- Only looking at the interest rate, not the APR

- Ignoring fees and closing costs

- Not checking their credit score before applying

- Picking the first lender they see

- Forgetting to ask about prepayment penalties

To avoid these, always ask for a full loan estimate and read the fine print.

How Home Equity Loan Rates Compare To Helocs

A HELOC (home equity line of credit) is different from a home equity loan. HELOCs usually have variable rates and let you borrow as needed. In 2024, HELOC rates range from 8%–12%, slightly higher than fixed home equity loans.

If you need a lump sum and want stable payments, a home equity loan is better. If you want flexibility and can handle changing payments, a HELOC may suit you.

When To Choose A Home Equity Loan

Home equity loans are best when:

- You need a large, one-time amount

- You want a fixed payment schedule

- You have strong equity and credit

If your needs are ongoing or uncertain, a HELOC or personal loan may be better. But for home improvement or debt consolidation, a home equity loan is often the smart choice.

Where To Find Up-to-date Rate Information

Rates change every week. To get the most current offers, check lender websites, financial news, and rate comparison sites. One reliable source is the Consumer Financial Protection Bureau. They track national averages and help you understand real costs.

Frequently Asked Questions

What Is A Good Home Equity Loan Rate In 2024?

A good rate is between 7% and 8.5% for borrowers with strong credit. Rates above 10% are common for lower credit scores or high LTV ratios.

How Does My Credit Score Affect My Rate?

A higher credit score means you’ll get a lower rate. Scores above 740 get the best deals, while scores below 650 may pay much more.

Can I Negotiate My Home Equity Loan Rate?

Yes, you can. If you have good credit and a strong relationship with your bank or credit union, ask for a better offer or discounts.

What Is The Difference Between Apr And Interest Rate?

APR includes the interest rate plus fees and costs. It’s a more accurate measure of what you’ll actually pay.

Are There Risks With Home Equity Loans?

Yes. If you can’t pay, you risk losing your home. Also, taking on too much debt can cause problems if your home’s value drops or your income changes.

Finding the best home equity loan rate takes research, patience, and some negotiation. By understanding what affects rates, comparing lenders, and watching out for hidden costs, you can make a smart decision and save money. Remember, your home is your most valuable asset — protect it by choosing the right loan and rate for your needs.

Read More:

- Best Personal Finance Software: Top Picks to Manage Your Money

- Financial Planning Advisor Near Me: Find the Best Local Experts

- Best Investment Apps for Beginners: Top Picks for 2024

- Retirement Planning Calculator Online: Secure Your Future Today

- Wealth Management Services for Beginners: Your Essential Guide

- Small Business Loan Pre Approval: Boost Your Funding Success

- Best Personal Loan Rates: How to Secure the Lowest APRs Today

- Debt Consolidation Loan Online: Simplify Your Finances Today