If you feel overwhelmed by multiple debts, you’re not alone. Many people face high-interest credit cards, personal loans, or medical bills, and struggle to keep up with payments. Managing different due dates and amounts can be stressful and expensive. That’s where debt consolidation loan online comes in—an option that can simplify your finances, lower your monthly payment, and help you take control of your debt. This guide covers everything you need to know, from how these loans work to mistakes to avoid and how to choose the right lender.

What Is A Debt Consolidation Loan Online?

A debt consolidation loan online is a personal loan you get from a bank, credit union, or online lender. You use the money to pay off other debts. Instead of many payments, you make one monthly payment, usually at a lower interest rate.

Online lenders make the process easier and faster. You can apply from home, check your rate, and get approved without visiting a branch. These loans are popular for people with credit card debt, medical bills, or payday loans.

Key Benefits

- Simplifies payments: Only one bill to pay each month.

- Lower interest rates: Many consolidation loans offer better rates than credit cards.

- Fixed terms: You know when the loan will be paid off.

- Improves credit score: Paying off credit cards can lower your credit utilization.

How It Works

- Apply for a loan online.

- Get approved and receive funds.

- Use the funds to pay off old debts.

- Repay the new loan monthly.

Many lenders allow you to pre-qualify without affecting your credit score. Approval depends on your credit history, income, and debt-to-income ratio.

Who Should Consider Debt Consolidation?

Debt consolidation loans are not for everyone. They are best for people who:

- Have several high-interest debts

- Can qualify for a lower interest rate

- Want to simplify their finances

- Have steady income to make loan payments

If you have poor credit or unstable income, you may not get the best rates. For some, other options like debt management programs or credit counseling work better.

Example: Comparing Debt Costs

Suppose you have three debts:

- Credit card: $5,000 at 20% APR

- Personal loan: $3,000 at 15% APR

- Medical bill: $2,000 at 10% APR

Total Debt = $10,000

Average Interest = 15.6%

If you consolidate into a loan at 10% APR, you could save hundreds in interest and pay off your debt faster.

How To Apply For A Debt Consolidation Loan Online

Applying online is simple, but you need to be prepared. Here are the main steps:

- Check your credit score: Most lenders want a score above 600.

- Gather documents: Proof of income, debts, ID.

- Compare lenders: Look at rates, fees, and terms.

- Pre-qualify: Many lenders let you check rates without a hard credit pull.

- Apply: Fill out the form, upload documents.

- Get approved: Review the offer before accepting.

- Pay off debts: Some lenders pay your creditors directly.

Online Lender Comparison

Here’s a quick look at three well-known online lenders:

| Lender | Min. Credit Score | APR Range | Loan Amount | Repayment Terms |

|---|---|---|---|---|

| SoFi | 680 | 6.99%–22.23% | $5,000–$100,000 | 2–7 years |

| Discover | 660 | 6.99%–24.99% | $2,500–$35,000 | 3–7 years |

| LightStream | 660 | 5.99%–20.99% | $5,000–$100,000 | 2–7 years |

Look for lenders with no origination fees, flexible repayment terms, and good customer reviews.

Important Factors To Compare

Before you choose a lender, focus on these key areas:

- Interest rate: Lower rates mean less interest paid.

- Fees: Some loans have origination or late fees.

- Repayment term: Shorter terms mean higher payments but less interest.

- Loan amount: Make sure it’s enough to cover all your debts.

- Customer service: Read reviews and check support options.

Sample Fee Comparison

Below is a comparison of typical fees:

| Lender | Origination Fee | Late Payment Fee | Prepayment Penalty |

|---|---|---|---|

| Marcus by Goldman Sachs | None | No fee | None |

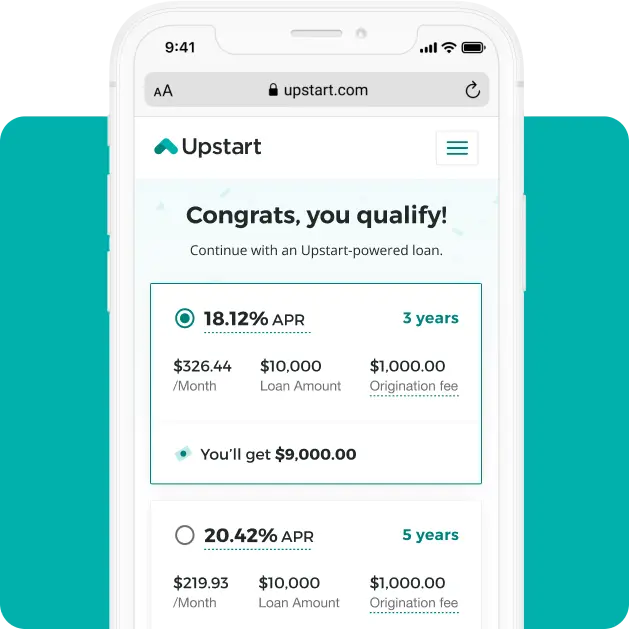

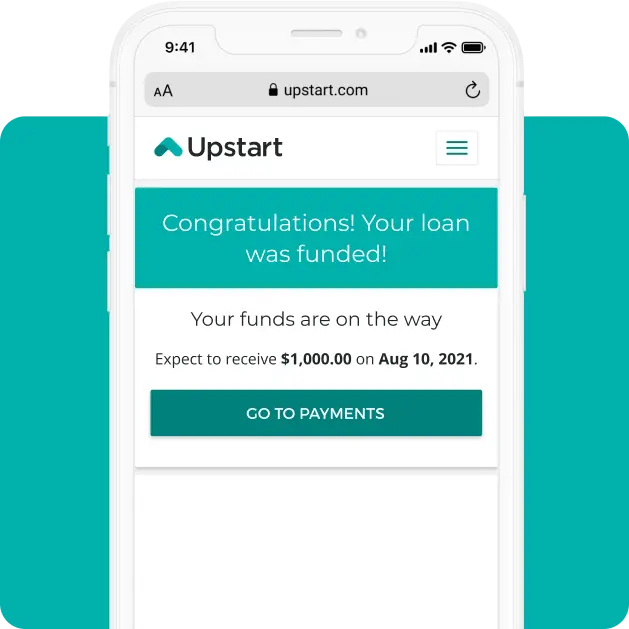

| Upstart | 0%–8% | $15 | None |

| LendingClub | 2%–6% | $15 | None |

Always read the fine print. Some lenders advertise low rates but charge high fees.

Common Mistakes To Avoid

Debt consolidation can help, but only if you use it wisely. Here are mistakes people often make:

- Not checking credit score: Applying with poor credit can lead to rejection or high rates.

- Ignoring fees: Some loans seem cheap but have hidden costs.

- Not budgeting: If you can’t afford the new payment, you risk default.

- Closing old accounts: Keeping old credit card accounts open can help your credit score.

- Borrowing more than needed: Only borrow what you need to pay off your debts.

Many beginners overlook the impact of their debt-to-income ratio. If your monthly debt payments are more than 40% of your income, lenders may decline your application. Another point people miss is the effect on their credit utilization. Paying off credit cards with a consolidation loan lowers your utilization, which can boost your score.

Pros And Cons Of Online Debt Consolidation Loans

Before you decide, consider the advantages and disadvantages.

Pros

- Convenience: Apply from home, quick approval.

- Competitive rates: Online lenders often have lower rates.

- Fast funding: Some lenders deposit money in 1–2 days.

- Flexible terms: Choose a term that fits your budget.

Cons

- Eligibility requirements: Good credit needed for best rates.

- Fees: Some lenders charge upfront costs.

- Risk of new debt: If you keep spending, you may end up with more debt.

- May affect credit score: A hard inquiry or new loan can temporarily lower your score.

Is Debt Consolidation Right For You?

Debt consolidation works best when you:

- Have high-interest debts

- Qualify for a lower rate

- Want to simplify payments

- Can stick to a repayment plan

If your debt is too large or your income is unstable, other options may be better. Consider talking to a financial advisor or credit counselor.

Real-life Example

Let’s look at Jane’s story. Jane had $12,000 in credit card debt at an average APR of 22%. Her minimum payments were $300 each month. She applied for a debt consolidation loan online and got a $12,000 loan at 8% APR for five years.

Her new monthly payment was $243. She saved $57 per month and over $7,000 in interest.

Jane’s experience shows the power of lower rates and fixed payments. She also learned that making extra payments helped her pay off the loan faster. Many people don’t realize they can pay more each month without penalty.

Tips For Success

To get the most from your debt consolidation loan:

- Shop around: Compare rates from at least three lenders.

- Check for prepayment penalties: Avoid loans that charge extra if you pay early.

- Don’t add new debt: Focus on paying off your consolidation loan.

- Monitor your credit: Track your score and report.

- Make extra payments: If possible, pay more than the minimum.

Alternatives To Debt Consolidation

Debt consolidation isn’t the only option. Here are others to consider:

- Balance transfer credit card: Moves your debt to a card with 0% intro APR for 12–18 months. Good for smaller amounts.

- Debt management plan: Works with a credit counselor to make one payment. May reduce interest rates.

- Home equity loan: If you own a home, you can borrow against it. Lower rates but your home is at risk.

- Snowball or avalanche method: Pay debts off one by one, starting with smallest or highest interest.

Each option has pros and cons. Choose what fits your situation.

How To Choose The Best Online Lender

Not all lenders are equal. Here’s what to look for:

- Transparent rates and fees

- Flexible repayment terms

- Good customer reviews

- Fast funding

- No prepayment penalties

Ask questions before you apply. Some lenders have strict requirements. Others are more flexible.

Lender Feature Comparison

Compare these features before choosing:

| Feature | Why It Matters |

|---|---|

| APR | Lower APR means less paid in interest. |

| Origination Fee | Fees can add to your loan cost. |

| Loan Term | Shorter terms = higher payments, less interest. |

| Direct Payment to Creditors | Simplifies the process, avoids mistakes. |

| Customer Support | Quick help if problems arise. |

Visit lender websites, read reviews, and use loan calculators to estimate payments.

Frequently Asked Questions

What Credit Score Do I Need For A Debt Consolidation Loan Online?

Most lenders require at least 600–650. Better rates are available for scores above 700. Some lenders accept lower scores but charge higher interest.

How Long Does It Take To Get Approved?

Approval can be same day or within a few days. Online lenders are faster than banks. Funding usually takes 1–5 business days.

Will Consolidating Debts Hurt My Credit?

Applying causes a hard inquiry, which may lower your score briefly. Paying off debts and lowering your credit utilization can improve your score over time.

What Debts Can I Consolidate?

You can combine credit cards, personal loans, medical bills, payday loans, and sometimes auto loans. Student loans usually require special consolidation options.

How Much Can I Borrow?

Most lenders offer $1,000–$100,000. The amount depends on your credit, income, and debt.

Debt consolidation loan online is a powerful tool for regaining financial control. By understanding how it works, comparing lenders, and avoiding common mistakes, you can simplify your payments, save money, and reduce stress. Always shop around, check your credit, and choose the best lender for your needs. If you want more details, visit the Consumer Financial Protection Bureau for official guidance. Remember, the goal is not just to pay off debt, but to build healthy money habits for life.

Read More:

- Best Personal Finance Software: Top Picks to Manage Your Money

- Financial Planning Advisor Near Me: Find the Best Local Experts

- Best Investment Apps for Beginners: Top Picks for 2024

- Retirement Planning Calculator Online: Secure Your Future Today

- Wealth Management Services for Beginners: Your Essential Guide

- Small Business Loan Pre Approval: Boost Your Funding Success

- Best Personal Loan Rates: How to Secure the Lowest APRs Today

- Home Equity Loan Rates Comparison: Find the Best Deals Today